Civil Litigation for Construction Professionals by Pete Fowler with Contributions by Mikala Glaza. Originally published in JLC’s Builder Guide - November 2023.

As a construction professional, you have probably heard the term “civil litigation.” With the large number of players involved in building projects—including developers/owners, designers, contractors, subcontractors, sub-subcontractors, suppliers, and more—it is nearly impossible to avoid a legal dispute at some point in your career. When two parties just cannot come to terms, they are likely to end up in civil litigation. And with so many parties involved, even the most simple building project can quickly become “complex litigation.”

From Bad to Worse:

An Example of How Construction Litigation Emerges

This is a painful example of a project type we have seen hundreds (seriously, hundreds) of times. A wealthy family wanting to build their dream home is friends with the spouse of a local custom builder. They reach out to the builder and hit it off immediately; on paper, it seems like a perfect match. They quickly reach an “agreement,” and construction begins with excitement. The builder receives the first few progress payments, and the process seems to be humming along.

Then, things take a turn for the worse. It turns out the “contract price” was really a budget. Every choice the owner makes—from roofing and siding to cabinets and flooring—exceeds the budget’s “allowance,” causing the price to rise weekly. The honeymoon is over. The tension is palpable. The owner and builder barely speak. Adding insult to injury, the owners begin to catch mistakes. Requested changes to bathroom three have been forgotten by the builder. The wrong plumbing fixtures are installed by seemingly incompetent subcontractors. Electrical outlets are in wacky places. Concerned about the situation, the owners audit the invoices and discover discrepancies. They hope these issues stem from negligence, but their concern grows as they notice that each “mistake” benefits the builder.

Construction limps toward completion. A certificate of occupancy is finally issued. The owners move in at last, but the home took twice as long to build and ended up costing twice as much as promised. Even worse, more problems emerge. The wood doors, which the owner insisted on placing in direct sunlight despite the builder’s warning that it would result in warping, have now begun to warp. The home automation system never works. Cooling bedroom two to a comfortable temperature turns bedroom four into an icy meat locker. The first rains come, and water pours into the home from the roof and windows.

The owners insist the builder immediately fix everything. As a precaution, the owners withhold final payment. The builder then stops responding to complaints, causing the owners to go ballistic and instruct their personal lawyer—who has no construction law experience—to file a lawsuit. The owner and builder are now engaged in litigation for years. —P.F.

Over the last 30 years, I have worked on thousands of litigated projects as a contracting and estimating expert witness. But I am not a lawyer, and a little knowledge is dangerous. For most lawyers, though, their depth of knowledge can actually make it difficult for them to explain the process simply. So, I worked with some lawyer friends to write this plain-language “map of the terrain” of civil litigation for non-lawyers who need to understand the process to help make smart business decisions.

Put simply, civil litigation is any noncriminal dispute resolved by a lawsuit using the court system. These cases are commonly settled before they reach the courtroom, but I will walk you through the entire process.

Common Types of Cases

Civil litigation covers a huge variety of cases, but there are common claim types building professionals face.

Construction defect litigation begins with allegations of physical problems and damage that are usually related to leaks or structural deficiencies but that can be related to any workmanship or performance problems on any building element (roofs, windows, walls, foundations, framing, plumbing, electrical, HVAC, and so forth). Defect allegations might be made during construction or not until many years after project completion. In some states, an entire “CD industry” has developed over the last 40 years, with attorneys and expert witnesses who work full time pursuing and defending these claims.

Personal injury (tort claims) is the type of lawsuit filed when an individual or business has been harmed by another. These claims include injury to someone, their reputation, or property due to fraud, negligence, or intentional acts. Common examples of this type of claim would be an auto accident, a premises liability slip, trip, or fall, a product defect, and many others. The goal is to seek compensation for physical, emotional, and financial damages incurred, including medical expenses, lost wages, pain and suffering, and other related losses.

Jobsite accidents are typically covered by workers’ compensation (see “Insurance Basics for Construction Professionals,” May/21) but, in many situations, a civil suit can also be filed against other parties that might have all or a portion of the responsibility due to negligence. In these cases, OSHA’s rules for multiemployer work sites often come into play.

Property claims refer to insurance or legal claims made to seek compensation for damage or loss to property. The damages are often caused by activities covered by insurance, such as fire, theft, vandalism, or natural disasters. Litigation is required only when the parties cannot agree on the extent and cost of the damages. For contractors, this can occur when they cause damage to property via a plumbing leak, a fire, equipment, or vehicles.

Contract claims arise from a party not fulfilling contractual obligations. These can be simple or very complex. When a contractor abandons an incomplete home-improvement project, unprovoked, it is simple. When a four-year renovation of a $10 million home for a television star goes bad, it is very complex. When a general contractor has a dispute with a trade contractor based on a poorly written contract with unclear terms, it is somewhere in between.

Subrogation claims are pursued by insurance companies to recover money for damages or losses caused by another party that the insurer believes is at fault. For example: If a contractor burns a house down sweating a copper pipe, the homeowner’s insurance will usually pay the claim and then seek reimbursement from the contractor. On large claims with unclear origins, this is sometimes contentious litigation requiring intensive work by expert consultants.

Equitable claims involve one party suing another to prevent a future, harmful act rather than suing for money. If there is a dangerous property, one party can ask the court to make the owner fix it. Or, if someone is doing something that could damage someone else’s property, the court can order them to stop. We have worked on many neighbor disputes over property lines or new construction blocking a view.

Peter D. Fowler

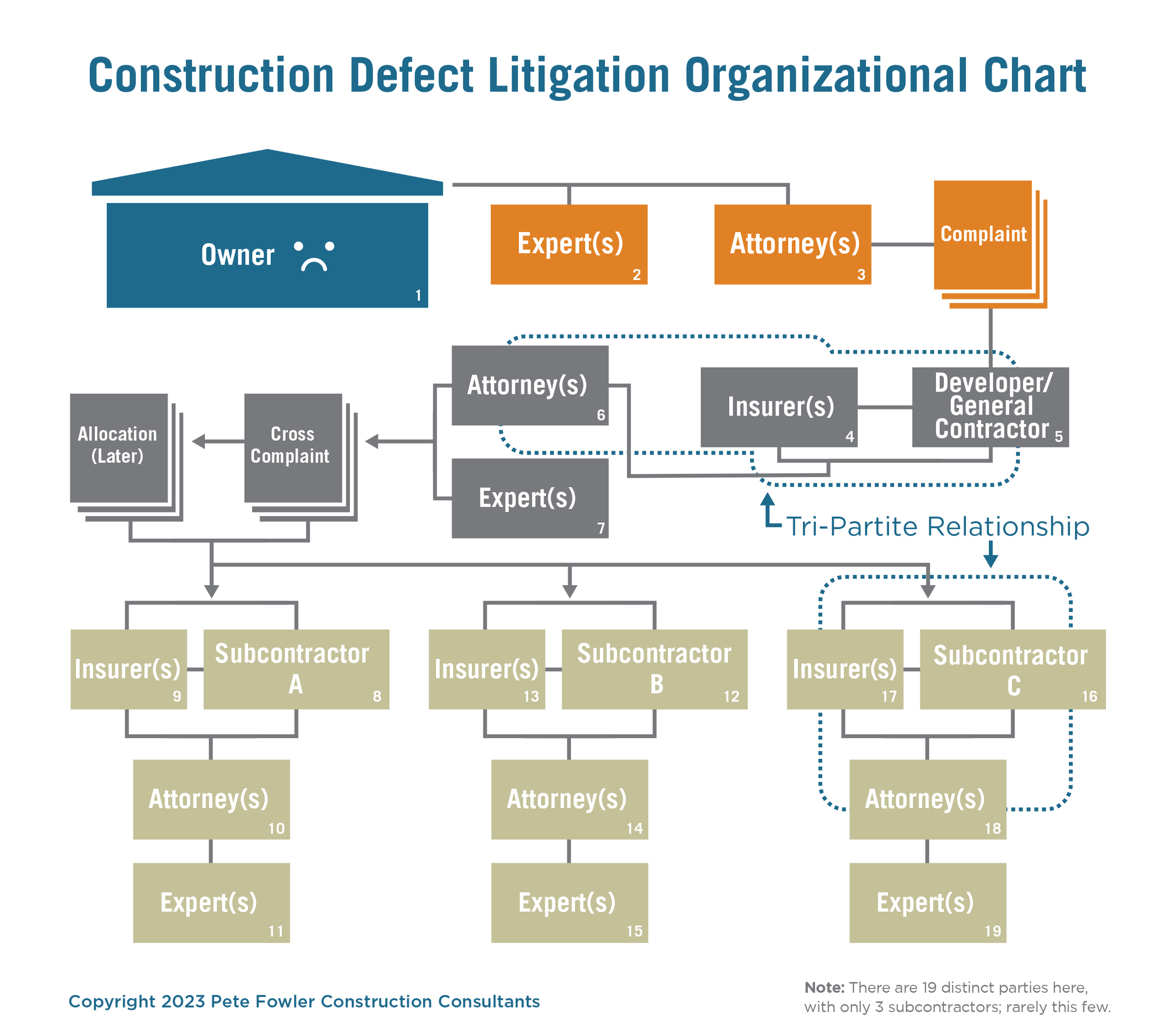

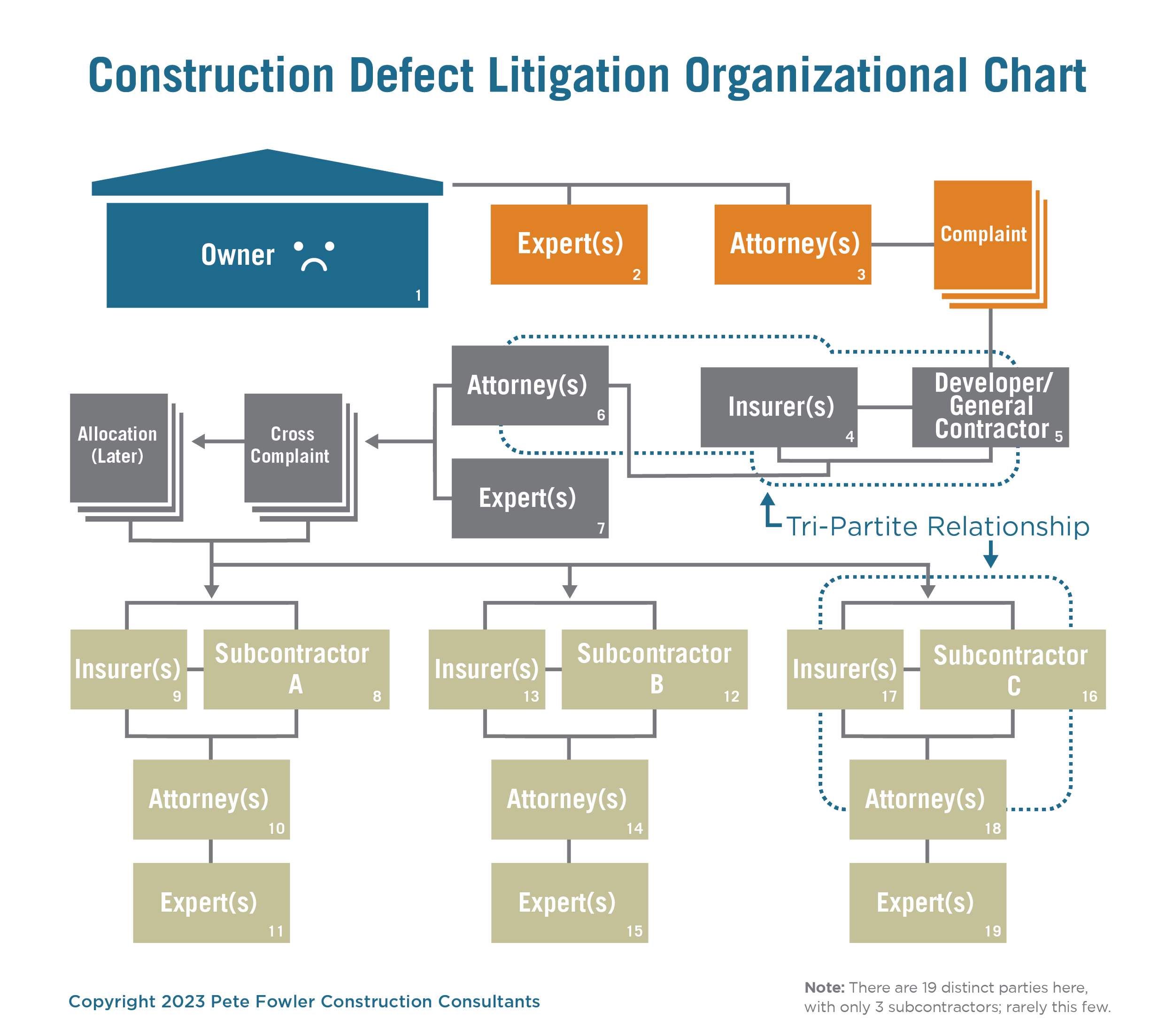

Example project organizational chart. When two or more players in a construction project cannot come to terms, they are likely to end up in civil litigation. Litigants will need to be clear on the roles and responsibilities of each player.

Roles and Responsibilities

As with any aspect of our business, a big-picture understanding of the roles and their responsibilities during civil litigation is an important requirement for construction professionals. Here are the basics:

A plaintiff is the person or company that initiates the lawsuit by filing a complaint against another party with the court. A plaintiff is also known as a claimant.

Attorneys represent plaintiffs, defendants, or cross-defendants. They are often referred to as “litigators” or “trial lawyers.” Attorneys generally manage all phases of litigation from beginning to end.

A defendant is a person or business that a lawsuit is filed against. It is important to remember that, in civil litigation, the defendant is accused of a civil wrong, not a criminal offense. These “wrongs” usually involve a failure to carry out legal duties, such as breaches of contract, or doing something they should not have, like causing damage.

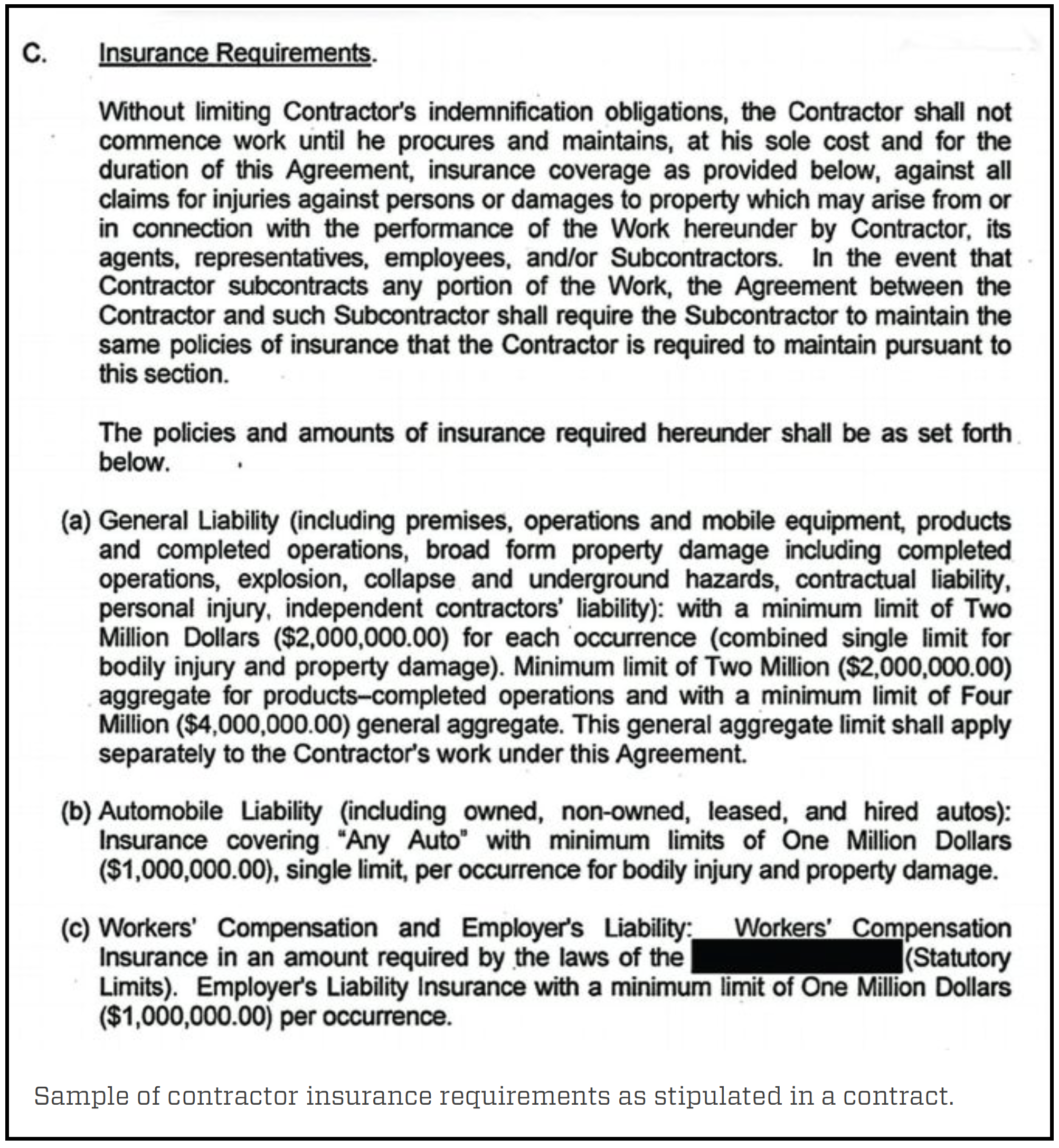

Insurance companies sell insurance policies to insureds (in our case, to contractors) that include a “duty to defend” as well as the “duty to indemnify.” The duty to defend provides the insured with legal representation when they are sued, so insurers hire and pay attorneys to represent insureds. Insurers typically do not pay to pursue claims as a plaintiff. The duty to indemnify pays for any legal judgments against insureds or, more often, to settle for damages that might be the insured’s responsibility. This is a complex topic far beyond the scope of this article. Suffice it to say, as soon as a claim is made or an accident happens, all parties should notify their insurance companies immediately.

Insurance professionals, namely claims handlers or “adjusters,” work for insurance companies and will be assigned to figure out what happened and how much the claim is worth. Early in my career, veteran insurance pros taught me that “a closed claim is a happy claim.” The common belief that these professionals are trying to pay less than the reasonable value of the claim is inconsistent with my experience. Their goal is usually to pay only what they believe the insurer owes, no more nor less.

Cross-defendant or third-party defendant is a third party being sued by a direct defendant in litigation, when the defendant believes the third party is partially or entirely responsible for the claims by the plaintiff. For example: A general contractor is sued by an owner for roof leaks. So the general contractor sues the roofing subcontractor. The roofing subcontractor is the cross- or third-party defendant (see chart, page 16).

A judge plays a different part depending on whether the trial is a jury trial or a bench trial (where a judge renders the verdict, not a jury). In both types, however, the judge is responsible for making sure everyone in the courtroom follows procedure, as sort of an all-powerful traffic cop. A judge should provide impartial, fair, and unbiased rulings throughout the case and is required to follow the law.

A jury includes between six and 12 community members selected to hear evidence and arguments during a trial. At the end of hearing evidence and arguments, they meet to deliberate and render a decision based on the “preponderance of the evidence.” This is in contrast to criminal cases, where the standard of proof is “beyond a reasonable doubt.” The jury decides if defendants are “liable” or “not liable” and determines the amount of damages.

A mediator is a neutral third party, often a lawyer, who facilitates communication and negotiation between disputing parties in an effort to reach a voluntary settlement. Unlike a judge or arbitrator, a mediator does not make binding decisions or impose solutions. Mediators in building claims help parties explore possible resolutions to their conflict, often by explaining the law, exposing weaknesses in the case and strengths of opposing parties’ cases, and calculating the costs of further litigation. This helps parties make a “business decision” rather than seek their version of “justice.”

An arbitrator is similar to a judge in that they oversee dispute resolution, but arbitration is private, outside of a courtroom, and less formal. The parties in the claim make arguments and present evidence and the arbitrator makes judgments on liability. The decision can be legally binding or nonbinding, depending on the language of the contract or situation.

Expert witnesses have specific knowledge, education, experience, specialized training, or some combination thereof in a field beyond what a normal person would have, and they can “aid the trier of fact” (judge and jury) in understanding the technical issues. There can be multiple experts on multiple topics in a single case. For example, a simple building litigation might have experts in leak investigation, product manufacturing and installation, repair costs, and contracting standards of care. Complex cases might have dozens of experts.

Litigation Stages

After a lawsuit is filed, civil litigation proceeds in specific stages.

Pre-filing is anything that happens before a party files a complaint to begin litigation. This is the time when the dispute arises and steps are often taken to resolve the dispute, even before lawyers are involved. Many contracts require mediation before a lawsuit can be filed.

Pleadings are the initial step of filing paperwork by each party in a lawsuit. Pleadings explain each party’s side of the dispute. The plaintiff will file a “complaint” with the court and must also deliver, or serve, the defendant with a copy of their complaint. The defendant will file an “answer,” which is a response to the complaint. A defendant might also file a “cross-complaint” against the plaintiff or additional cross-defendants or third-party defendants.

Discovery is a phase that involves gathering and sharing information, both from parties involved in the case and from third-party sources. Discovery can include requests for copies of documents, deposition of witnesses, and written requests for admission. This is often the longest, most complicated, and most expensive phase in the litigation process, so it is best to have a discovery plan. This should entail identifying the primary issues, determining what needs to be proven to win, deciding if the goal is alternative dispute resolution or trial, and strategizing the most time- and cost-effective path forward.

Pre-trial phase involves preparing for trial. This may include getting evidence in order, preparing witnesses for testimony, having settlement discussions, and offering motions to resolve the case or narrow the issues brought to trial. This phase is typically expensive and stressful for everyone involved.

Trial is where evidence and arguments are formally presented to judge and jury. There are a lot of rules and formality. Both parties give opening statements that are a brief overview of their arguments. Witnesses give sworn testimony, and both sides present evidence, first the plaintiff, then defendants. Ultimately, the judge and/or jury will decide the outcome. It is stressful and difficult and therefore expensive. This is why only 1% or fewer civil litigation cases make it to or through trial. In 99% of cases, trial is best avoided.

Jury trials have a judge to make sure the parties follow the law and to decide what evidence and witnesses can be presented. The judge will also provide the jury with instructions about the law to guide their decision on a verdict (outcome) and the award of damages (usually money).

Bench trials have no jury; the judge is responsible for hearing the evidence and arguments, determining liability, and setting the judgment amount.

Post-trial phase usually involves the prevailing party filing a motion to request the court to order the losing party to pay their costs and fees associated with the case, including costs of the trial. These awards may or may not include attorney’s fees. The post-trial phase can also involve appeal of the case. If the losing party does not agree with the court’s decision, it can file an appeal to a higher court for a second look at the case. These appeals are usually granted only if the higher court finds a legal error, not because of factual evidence.

Peter D. Fowler, adapted by JLC

All civil litigation has a plaintiff, plaintiff attorney, defendant, and defense attorney. Building-related claims often have many cross-defendants (commonly trade contractors and suppliers) and their attorneys, as well.

Alternatives To Litigation

For good reason, most civil litigation is settled before trial. This is usually more cost-effective and time-efficient.

Settlement occurs any time plaintiffs and defendants come to terms to end a dispute before a formal verdict by judge or jury. This often happens during the discovery phase after some facts come to light that inspire the parties to settle instead of going to trial.

Mediation involves a neutral third party (mediator) working with plaintiffs and defendants to negotiate a settlement. This is a nonbinding forum. Sometimes, judges are available as mediators but, more often, lawyers with specialized mediation training are used as the neutral party. All parties, sometimes all together, present their information to the mediator but, more often, the mediator meets with each side individually. The entire process is confidential, and the discussions cannot be used in litigation or trial.

Arbitration, like mediation, involves a neutral third party (arbitrator) to resolve the dispute but is more formal than mediation. It is a form of privatized litigation intended to be faster and cheaper than civil litigation. Many contracts contain an arbitration clause requiring disputes to be resolved through binding arbitration, rather than litigation. Arbitration can be binding or nonbinding.

Pete Fowler, Chief Quality Officer, Pete Fowler Construction Consultants